Credit Cards in Islamic Finance: Halal or Haram?

Interest vs. Utility: The Modern Muslim’s Credit Card Dilemma

Navigating modern finance while staying true to Shariah principles can feel like walking a tightrope, especially when it comes to credit cards. Are they a helpful tool for building a credit score, or a trap involving Riba?

The answer isn't a simple "yes" or "no." It depends on how the card is structured and, more importantly, how you use it. Here is a breakdown of the debate, the conditions for use, and the practicalities of credit cards in an Islamic context.

The Core Debate: Halal vs. Haram

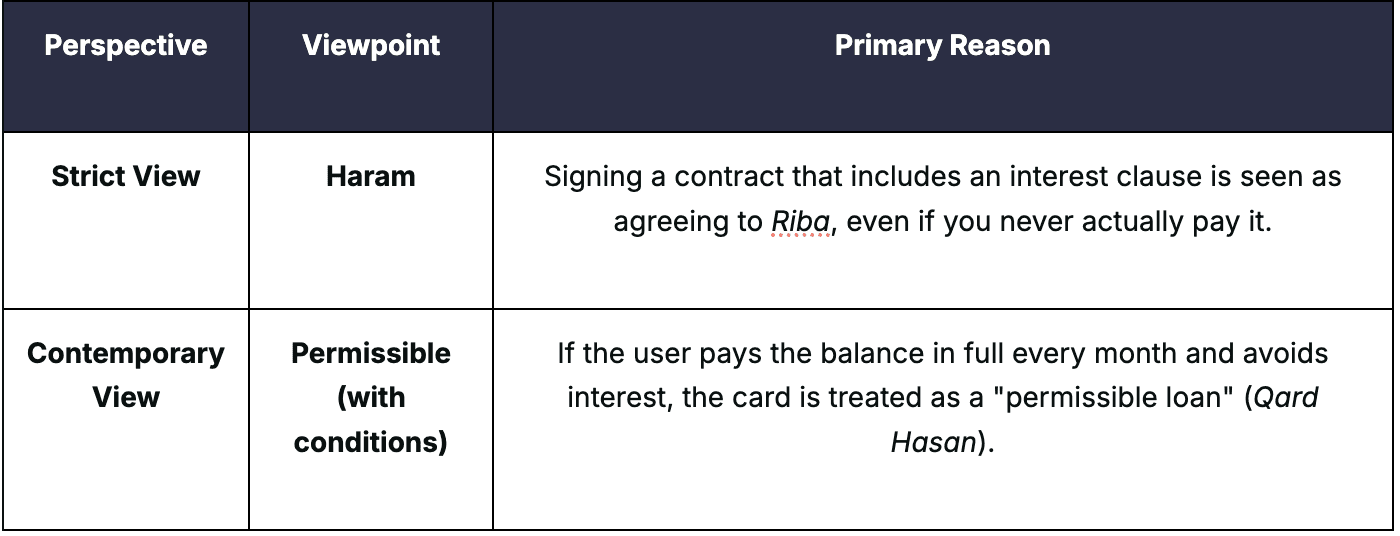

The primary concern with credit cards is the interest (Riba). In Islam, paying or receiving interest is strictly prohibited. Because a standard credit card contract requires you to agree to pay interest if you carry a balance, some scholars view the mere act of signing the contract as problematic.

However, many contemporary scholars take a more pragmatic view, focusing on the intention and the outcome.

Two Schools of Thought

4 Reasons Why Credit Cards are Often Used by Muslims

Despite the debate, there are several reasons why many Muslims find credit cards permissible and even necessary in today's economy:

1. Interest-Free Borrowing

In Islamic finance, borrowing money is allowed as long as there is no "increase" (interest). If you use a credit card and pay the statement balance in full before the due date, you are effectively receiving an interest-free loan for 21–30 days.

2. The Reality of Late Fees

Critics point to late fees as a form of interest. However, proponents argue that late fees are now standard in almost all modern contracts (utility bills, rent, phone plans). If we disqualified every contract with a penalty clause, it would be nearly impossible to function in a modern economy.

3. Essential Consumer Protection

Credit cards offer "Section 75" style protections (depending on your region) that debit cards do not. This includes:

Fraud Protection: Easier to dispute unauthorized charges.

Travel Benefits: Better exchange rates and built-in travel insurance.

Online Security: A layer of safety when shopping on international websites.

4. Revenue Diversification

Credit card companies don't just make money from interest. They earn "Interchange Fees" (transaction fees paid by the merchant). This means even if you never pay a cent of interest, the company still profits from the service they provide to the store, which some see as a legitimate service fee.

Guidelines for Halal Credit Card Usage

If you choose to use a credit card, you must manage it with extreme discipline to stay within Shariah boundaries. Follow this checklist to ensure your usage remains ethical:

Set Up Autopay: Always set your account to pay the Full Balance automatically. This eliminates the risk of accidentally triggering interest charges.

Avoid "Cash Advances": Taking cash out of an ATM with a credit card usually triggers interest immediately with no grace period. This is strictly avoid-worthy.

Monitor "Halal" Rewards: Some scholars suggest that "Cashback" is permissible as it is a gift (Hiba) from the bank, but you should avoid rewards specifically linked to haram industries.

Use it for Utility, Not Luxury: Use the card as a tool to build your credit score (which is necessary for getting a Halal Mortgage later) rather than a way to buy things you cannot afford.

Conclusion: A Tool for Responsibility

In the world of Islamic finance, your intention (Niyyah) and your discipline are paramount. While a credit card has the potential to involve Riba, it also serves as a vital tool for financial security and building a credit history in the West.

If you are uncomfortable with traditional credit cards, look for Halal alternatives or prepaid cards that offer similar protections without the interest-bearing contract.